Wild Ride in Markets this Week

April 10, 2025

As the famous quote by Vladimir Lenin says, “there are decades where nothing happens; and there are weeks when decades happen.” This has sure been one of those weeks and has reminded me of being on a less than enjoyable roller coaster ride.

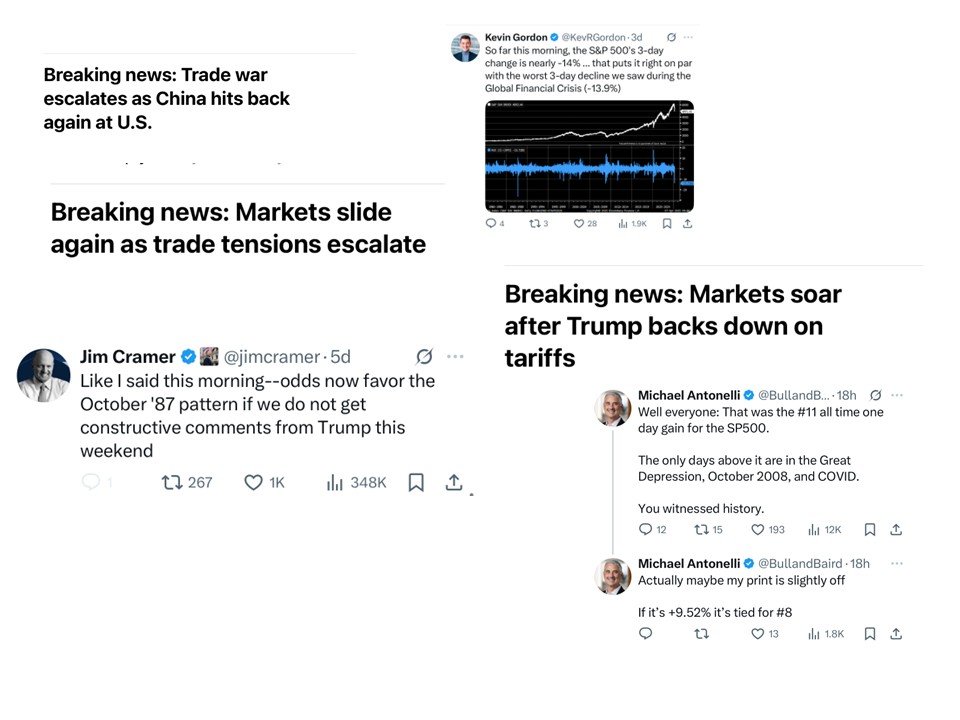

If you haven’t been keeping up with the news flow and market action, first off – lucky you (ha!) Here’s a snapshot of a few of the news headlines and market commentary tweets from the days following President Trump’s tariff announcement.

Confused? Welcome to the club of virtually every investor (and perhaps citizen). It has been a volatile and confusing few days but here’s the cliffs note version of what has occurred

The Start – President Trump announced a sweeping tariff program on April 2nd. These tariffs were labeled reciprocal but in fact were calculated using a formula based on trade deficits, resulting in tariffs being placed on over 70 countries including allies of the US as well as countries with whom the US had a trade surplus (they received a minimum tariff rate of 10%). As these figures were far higher and far more sweeping than anticipated, markets were not impressed

Initial Reactions – Markets reacted very negatively to this announcement in the after hours session and continued a steady decline for the following days. At first, the losses were focused in the equity markets (with the higher growth areas such as the NASDAQ (tech/growth heavy companies) and the Russell 2000 (smaller cap companies which tend to be more sensitive to economic downturns) being hit the hardest).

In the initial days, the only saving grace for investors (and likely for the administration) was that the bond market was reacting as expected in a “crisis.” The US bond market tends to be the safe haven in times of economic uncertainty (based on the belief the US will always be able to repay its debt), and as a result, demand for US debt rises during volatile times (the so called “flight to safety”). This increased demand pushes down the prevailing interest rates on US debt (if more people want what you’re selling, you don’t have to pay them as much to buy it). This move was evidenced by the US 10-year rate falling below 4% in the days right after the announcement. This was good news for investors (as falling rates increases value of fixed income holdings, offsetting equity losses in a balanced portfolio) as well as for borrowers and economic activity (as lower rates make consumers more likely to borrow, buy homes, spend money, etc)

Contagion – Market commentators started to panic on Friday and into the weekend. Major investment banks revised their odds of a recession. Strategists cut their once sky-high price targets for US indexes. Many predicted a “black monday” repeat. Hedge fund managers (like Bill Ackman), well known political figures (like Larry Summers, former Treasury secretary), and some current/former CEOs (like Lloyd Blankfien) encouraged President Trump to pause the tariffs and refocus efforts on selected countries (namely – China). The President pressed on all while ratcheting up the fight with China by placing retaliatory tariffs on top of their retaliatory tariffs

Mass Contagion – On Tuesday of this week, something seemed to break the “hold the line” strategy of the Administration just as the massive tariffs took effect – and that something was the bond market. Rates on US debt started to move sharply higher in Tuesday’s session. This was highly unusual (see above discussion on “flight to safety” dynamic) and does not bode well for the US, as it would have to pay higher rates of interest to fund its deficit, as well as saddle its citizens and companies with a higher cost of capital. In Trump’s own words on Wednesday (when talking about the bond market) on Tuesday – “I saw last night where people were getting a little queasy”

(Some) Relief – Mid-day Wednesday, markets and the surrounding firestorm got some relief as President Trump announced a 90-day pause on all tariffs (excluding China). He reiterated deals would be taking place to benefit the US (giving him a needed victory/off ramp) and refocused the efforts on China (which many believed was the initial target to begin with). Equity and bond markets stagged a huge rally.

Back down – As of Thursday, as I write this, markets are giving back some of the record setting gains as the back and forth continues with China and discussions of negotiations with other countries continues but nothing has come to bear as of yet.

Where does this leave us? Congress passed the Administration’s budget bill today. March’s CPI report (released today with very little fanfare) showed encouraging inflation results which the markets shrugged off as the impact of tariffs and declining confidence have yet to be felt. Earnings season kicks off next week, where we will hear first hand from companies and CEOs. And endless stream of predictions and forecasts dominate the business news. In sum, the roller coaster ride continues.

The truth of it is that investing over the long term has always been – and will always be – a roller coaster ride. Fortunately, for the majority of the time, we are on a ride that more closely resembles “It’s a Small World” boat cruise at Disney World. And for a very small portion of our investing journey we get trapped on a ride that echoes the “Tower of Terror” at Hollywood Studios!

This bumpy part of the ride (ie: volatility and declining values) is the price we must pay to achieve the long term compounding of wealth. It never feels good at the time (never!) but up until now, the ride has always smoothed out eventually, and there is no use thinking this time will be different. No matter how much we dislike it and no matter how bumpy it gets, we must stay seated and we must stay on the ride. As you can see from Wednesday’s stunning reversal, getting off the ride in the middle is the one sure fire way you truly get hurt.

So, buckle up. We’re not thru this particular bumpy part yet but the good news is none of us have gotten off yet – giving us the incredible opportunity and privilege to once again reach the calmer section of the ride.

Onward we go,

Leave a note