Client Question: What’s a Recession?

May 1, 2025

I talked with a client this week about a “hot topic” in the news as of late – what exactly is a recession? This is an important topic to understand so let’s take a look.

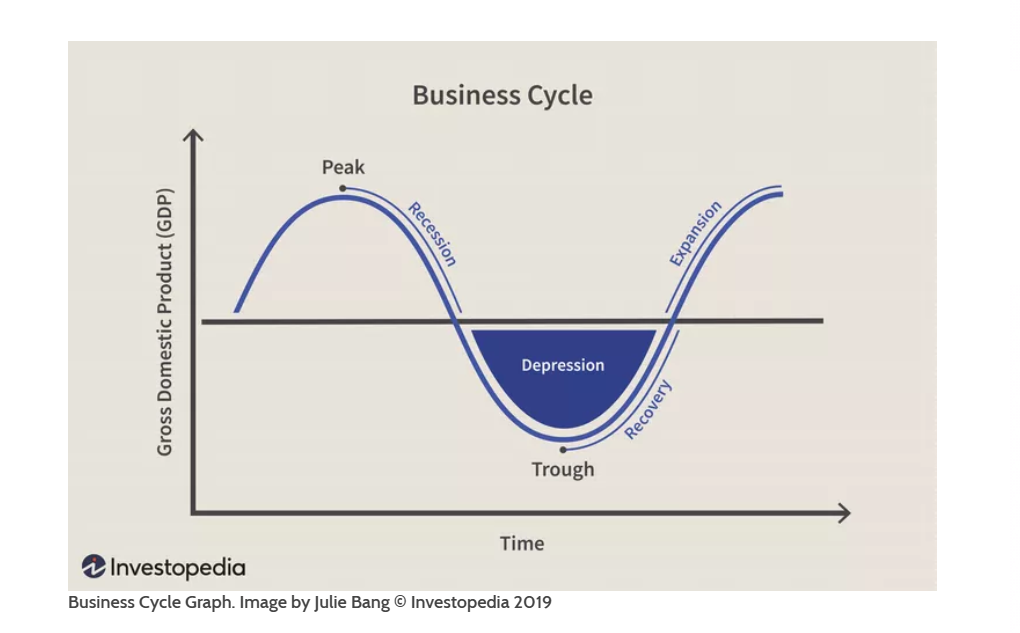

Before diving into recession definition, let’s look at the broader business cycle. This chart does a nice job showing the stages. As it relates to the US economy, we had a brief recession in 2020 and since that point, growth (GDP) has been increasing and we’ve been in an expansionary period. At some point, that growth peaks, growth falls, and after a period of time, the cycle starts over again.

In recent months, with the ongoing political uncertainty regarding tariffs, concerns over a recession have risen. What defines a recession? Many believe it’s defined as two consecutive quarters of negative GDP (and if you’re keeping score, we already have one quarter of negative growth (as discussed in more detail here)).

However, in reality, since 1978, the official arbiter of recessions has been the National Bureau of Economic Research (NBER), which provides start/end dates by month for recessions, always in retrospect. And perhaps surprisingly, the NBER’s definition is not two consecutive quarters of negative gross domestic product readings.

The actual definition per the NBER is “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” The NBR looks at three criteria for each contraction —depth, diffusion, and duration. The NBR looks at many data points, including but not limited to real personal income less transfers, nonfarm payroll employment, real personal consumption expenditures, wholesale-retail sales adjusted for price changes, employment as measured by the Bureau of Labor Statistics’ household survey, and industrial production.” Per the NBER, they have “no fixed rule about what measures contribute information to the process of how they are weighted.”

Oftentimes, a recession by the NBER may coincide with two negative GDP quarters but it’s important to keep in mind that is not the only criteria.

Why does tipping into a recession matter? It represents a slowdown in growth, which can lead to lower earnings, lower wages, lower equity prices, and many other less than ideal facts for the country and its citizens. The good news however is that recessions are part of the cycle and eventually, they too pass (think back to 2007/2008 and 2020 (a much shorter recession but still a recession)

The trend in GDP, as well as many other economic factors, will be closely watched as we move thru 2025. A recession is always possible and unless we see some more progress on trade and a quick rebound in spending and confidence, it may remain increasingly probable.

Leave a note